ASSETS

What Is an Asset?

The International Financial Reporting Standards (IFRS) defines an asset as “a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise.”

Put another way, assets are valuable because they can generate revenue or be converted into cash. They can be physical items, such as machinery, or intangible, such as intellectual property. Assets are reported on a company’s balance sheet, one of its key financial statements.

Types of Assets

Assets can be classified based on a number of criteria. For companies, the correct classification is critical to financial reporting and evaluating the business’s financial health. Typically, assets are valued by the expected future cash flows they represent in their current condition, according to the IFRS.

Personal: Soft personal assets, such as intellect, wit or a winning smile are different than personal financial assets, which contribute to an individual’s or household’s net worth. Examples of personal financial assets include cash and bank accounts, real estate, personal property such as furniture and vehicles, and investments such as stocks, mutual funds and retirement plans.

Business: Business assets deliver value to a company because they can be used to produce goods, fund operations and drive growth. Assets include physical items such as machinery, property, raw materials and inventory, and intangible items like patents, royalties and other intellectual property. Companies account for their assets on their balance sheet and categorize them based on a set of criteria that reflect their liquidity, or how readily they can be converted to cash, as well as whether they are physical or nonphysical assets and how they’re used to derive value.

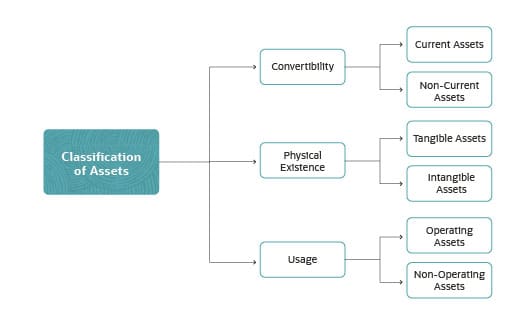

Convertibility: it refers to how readily a business can convert an asset to cash. Assets that are likely to be turned into cash within one fiscal year or operating cycle are called current assets. While any asset can be converted into cash within 12 months if the price is sufficiently discounted, current assets only include assets that are expected to be converted into cash within 12 months.

Current assets include:

- Cash and cash equivalents, such as treasury bills and certificates of deposits.

- Marketable securities, such as stocks, bonds and other types of securities.

- Accounts Receivables or sales to customers on credit that must be paid in the short term.

- Inventory, or the salable goods and materials a company has on hand.

Non-current assets are items that may not be readily converted to cash within a year. Examples of such assets include facilities and heavy equipment, which are listed on the balance sheet, typically under the heading property, plant and equipment (PP&E). Not all companies use the term “PP&E” on their balance sheet—they may instead list non-current assets under the heading fixed assets, long-term assets or simply non-current assets.

Physical existence: Assets that have a physical existence are called tangible assets. They include cash, PP&E, inventory, raw materials or tools and office supplies. Tangible and intangible assets that are expected to provide an economic benefit beyond the current year, such as manufacturing equipment or buildings, are called or “long-lived” assets.

Intangible assets, as the name implies, lack a physical presence. Examples of intangible assets include right of use assets, patents, copyrights and trademarks, the value of which can sometimes be difficult to quantify.

Some tangible and intangible assets are referred to as wasting assets, or assets that decline in value over a limited life span. Tangible assets that qualify as wasting assets include manufacturing equipment and vehicles, which wear down or become obsolete over time. Intangible assets such as patents also qualify as wasting assets because they have a limited lifespan before they expire. To reflect wasting assets’ reduction in value over time, accountants reduce the assets’ value on the balance sheet by applying depreciation (for tangible assets) or amortization (for intangible assets).

Usage: Finally, an asset can be classified as operating or non-operating based on how a company uses it. Operating assets are necessary to the primary operations of a business, such as cash, inventory, factories and patents. For a mining company, heavy equipment qualifies as an operating asset, as does a manufacturer’s production equipment.

Non-operating assets are not necessary for funding business operations but have other peripheral value. Examples include short-term investments, marketable securities, interest from deposits and administrative computers.

Examples of Assets

There are a wide variety of assets that businesses might have to perform at their highest level. They include:

- Cash and cash equivalents

- Accounts receivable (AR)

- Marketable securities

- Trademarks

- Patents

- Product designs

- Distribution rights

- Buildings

- Land

- Mineral rights

- Equipment

- Inventory

- Software

- Computers

- Furniture and fixtures

Three Key Properties of Assets

For something to be considered an asset, it must have three properties:

- Ownership: First, a company must have ownership or control of the asset. This enables the company to convert the asset into cash or a cash equivalent and limits others’ control over the item. Note, right of use assets aren’t always convertible. Lease agreements often stipulate that the lease cannot be transferred or sold. The ownership property is important when considering an asset’s informal meaning versus its technical meaning. For example, companies often say their employees are their “greatest asset,” but in terms of accounting, companies don’t have true control over them—employees can easily leave for a new job.

- Economic value: Second, an asset must also provide economic value. All assets can be sold or otherwise converted to cash, except for some right of use assets such as lease agreements. In that way, assets can be used to support production and business growth.

- Resource: Finally, an asset must be a resource, which means it has or can be used to generate future economic value. This generally means that the asset can create future positive cash inflows.

Three Classifications of Assets

Business assets can be divided into three different categories based on their convertibility, physical existence and usage. What are these three types of assets?

- Convertibility describes how easily assets can be converted to cash.

- Physical existence describes whether an asset physically exists or is intangible.

- Usage describes the purpose of an object as it relates to business operations.

How Do I Know If Something Is an Asset?

An asset is something that provides a current, future, or potential economic benefit for an individual or other entity. An asset is, therefore, something that is owned by you or something that is owed to you. Therefore, a $10 bill, a desktop computer, a chair, or a car are all assets. If somebody owes you money, that loan is also an asset because you are owed that amount (even though the loan is a liability for the one paying you back).

What About Non-physical Assets?

Intangible assets provide an economic benefit to somebody, but you cannot physically touch them. These are an important class of assets that include things like intellectual property (e.g., patents or trademarks), contractual obligations, royalties, and goodwill. Brand equity and reputation are also examples of non-physical assets that can be quite valuable. Some financial assets, such as shares of stock or derivatives contracts are also intangible.

Is Labor an Asset?

No. Labor is the work carried out by human beings, for which they are paid in wages or a salary. Labor is distinct from assets, which are considered to be capital.

Comments

Post a Comment